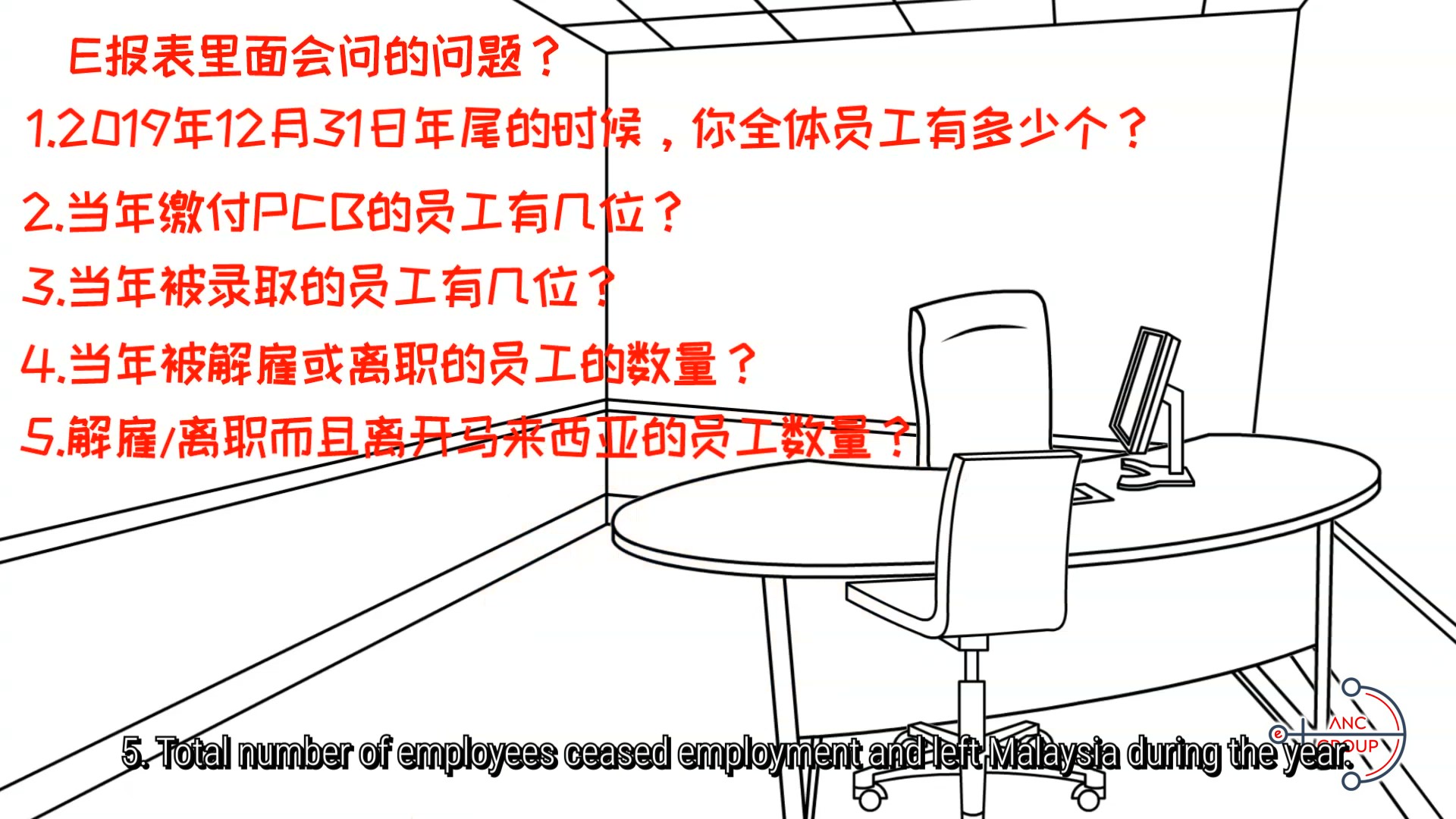

e-Invoicing: Why issuing self-billed e-Invoice matters now?

![]()

- What is self-billed e-Invoices?

When a sale or transaction is concluded, an e-Invoice is issued by Supplier to recognise income of the Supplier (proof of income) and as a record for purchases made / spending by Buyer (proof of expense).

However, there are certain circumstances where another party (other than the Supplier) will be required to issue a self-billed e-Invoice. - What are the transactions that require self-billed e-Invoices?

For e-Invoice purposes, Buyer (assumes the role of Supplier) and issue self-billed e-Invoices for the following transactions:否 Transaction Supplier 买方 1 Payment to agents, dealers and distributors Agents, dealers and distributors Taxpayer that makes the payment 2 Goods sold or services rendered by foreign suppliers Foreign seller Malaysian Purchaser 3 Profit Distribution (dividend distribution) Recipient of the distribution Taxpayer that makes the distribution 4 E-Commerce Merchant, service providers E-Commerce / Intermediary Platform 5 Pay-out to all betting and gaming winners Recipient of the pay-out Licensed betting and gaming provider 6 Acquisition of goods or services from individual taxpayers who are not conducting a business Individual taxpayer providing goods or services Person acquiring goods or services 7 Interest Payment Recipient of interest payment Taxpayer that makes the interest payment 8 Claim, compensation or benefit payments from the insurance business of an insurer Policyholder / Beneficiary Insurer - Can I issue self-billed e-Invoice for any circumstance that is not listed under Section 8.3 of the e-Invoice Specific Guideline?

No, please note that issuance of self-billed e-Invoice is only permitted for circumstances that are provided under Section 8.3 of the e-Invoice Specific Guideline.

- Can I issue self-billed e-Invoice if my supplier did not issue e-Invoice to me?

Issuance of self-billed e-Invoice is only permitted for circumstances that are provided under Section 8.3 of the e-Invoice Specific Guideline. Where the transaction does not fall within Section 8.3 of the e-Invoice Specific Guideline, taxpayers are not allowed to issue self-billed e-Invoice.

- Is there a way to better understand the mechanism, implementation, self-billed for e-Invoice?

Yes, you can gain further insights into the e-Invoice mechanism and workflow by referring to the official guidelines published by the Inland Revenue Board of Malaysia (IRBM).

-

-

- Download e-Invoice Guideline Version 4.0 (published on 04 October 2024)

- Download e-Invoice Specific Guideline Version 3.1 (published on 04 October 2024)

- View e-Invoice Illustration Guide (Updated on 11 September 2024)

-

You may also consider attending e-Invoice training courses for detailed guidance.

For more information or to register, please visit the contact link below: ANCGroup_E-Invoice Courses Contact.

ANC Group – Your Personal Tax Advisor

Tax consulting is the core service of ANC Group. Our tax professionals provide clients with comprehensive tax support and guidance. We offer tax consulting and compliance services for expatriates, entrepreneurs, and listed and non-listed companies.

Our tax consulting services include business tax, transaction tax, personal tax, and corporate income tax. We don’t just guide you in interpreting and applying complicated taxation rules, but to explore new opportunities and business trends.

ANC Group keep you abreast with Malaysia tax updates and any changes in the local regulations.

We work closely with industry specialists, authorities, and associated professionals within ANC Group to provide the best-in-class integrated tax planning solutions. ANC specialists coordinate the accounting and taxation services to bring your business to success.

[vc_btn title=”Get a Quote” color=”orange” size=”lg” link=”url:%23Footer|title:Footer||” el_id=”buttonGetQuoteTaxService”]