简介

Unabsorbed business loss Malaysia(简称 UBL)让企业可以将往年未使用完的业务亏损结转至未来年度,用于抵扣未来业务收入。掌握 UBL 在《所得税法》下的运作方式,有助于企业进行妥善税务规划与合规。

什么是 Unabsorbed Business Loss(UBL)?

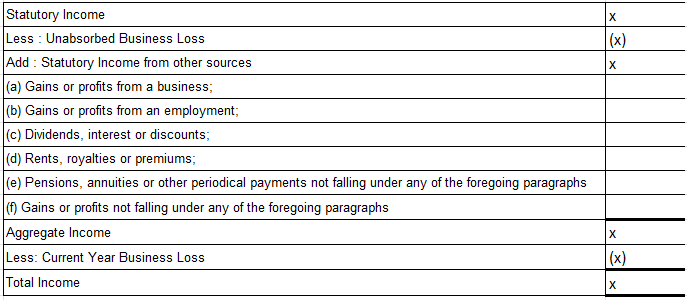

若企业在过去课税年度(例如 YA 2017)产生了业务亏损,而在该年度未完全抵消,则会形成 UBL,并允许结转至下一课税年度(如 YA 2018)以及之后的年度,直到完全抵扣为止。 UBL 只能抵扣业务收入,不可用于薪资、利息或股息等非业务收入。

当年业务亏损:可抵扣 vs. 不可抵扣

当年度的业务亏损只能抵扣 同一课税年度的业务收入,不可用于抵扣非业务来源的收入。 此规定确保不同收入类别的税务计算保持一致与公平。

亏损结转机制:规则与限制

| 课税年度 | 亏损处理方式 |

| 有业务亏损年度 | 亏损结转为 UBL |

| 之后的课税年度 | 可用来抵扣未来业务收入 |

| 永久(若未完全抵扣) | 继续结转,直至完全吸收 |

Important如未来年度没有业务利润,UBL 将持续累积,不会失效。

示例:

假设一家公司情况如下:

- 2018 评税年度(YA 2018)— 业务亏损 RM X(无业务利润)→ 成为未利用业务亏损(UBL)

- 2019 评税年度(YA 2019)— 有业务利润 → 2018 年的未利用业务亏损(UBL)可用于抵消利润

如果经过数年仍未吸收该亏损,根据现行规定,该亏损将无限期结转下去。

为何对企业重要?

- 协助企业度过低利润年份

- 平衡不同年度盈利波动

- 必须保存税务记录与账目以支持申报

关键要点

- UBL 可无限期结转,直至完全吸收

- 只能抵扣业务收入

- 当年业务亏损也只能抵业务收入

- 必须保留良好账目以支持申报

常见问题

Q: UBL 可抵扣出租收入吗?

A: 不可以,只能抵扣业务收入。

Q: UBL 结转有年限限制吗?

A: 目前没有限制,但需确保为业务收入来源。

Q: 若企业同时有业务收入与非业务收入?

A: 只能抵扣业务收入部分。

ANC Group – Your Personal Tax Advisor

Tax consulting is the core service of ANC Group. Our tax professionals provide clients with comprehensive tax support and guidance. We offer tax consulting and compliance services for expatriates, entrepreneurs, and listed and non-listed companies.

Our tax consulting services include business tax, transaction tax, personal tax, and corporate income tax. We don’t just guide you in interpreting and applying complicated taxation rules, but to explore new opportunities and business trends.

ANC Group keep you abreast with Malaysia tax updates and any changes in the local regulations.

We work closely with industry specialists, authorities, and associated professionals within ANC Group to provide the best-in-class integrated tax planning solutions. ANC specialists coordinate the accounting and taxation services to bring your business to success.

If you need professional tax advisory services regarding the Malaysia Income Tax Act 1967, our team is ready to assist you. Contact us here to discuss how we can support your business.